By John Allen November 27, 2025

Restaurant payment processing is now just as important as your menu and your service. In the U.S., most diners expect to pay with cards or digital wallets, and they get annoyed when checkout is slow or limited.

At the same time, fees, fraud, and compliance rules have never been more complex. Getting restaurant payment processing right means higher tips, faster table turns, and better margins. Getting it wrong means lost sales, chargebacks, and angry reviews.

In this guide, you’ll learn exactly how restaurant payment processing works behind the scenes, which payment methods you should support, how to keep fees under control, and how to stay compliant with changing rules like PCI DSS 4.0.

We’ll also look ahead at future trends so you can choose payment processing for restaurant operations that won’t be outdated in two years.

What Is Restaurant Payment Processing?

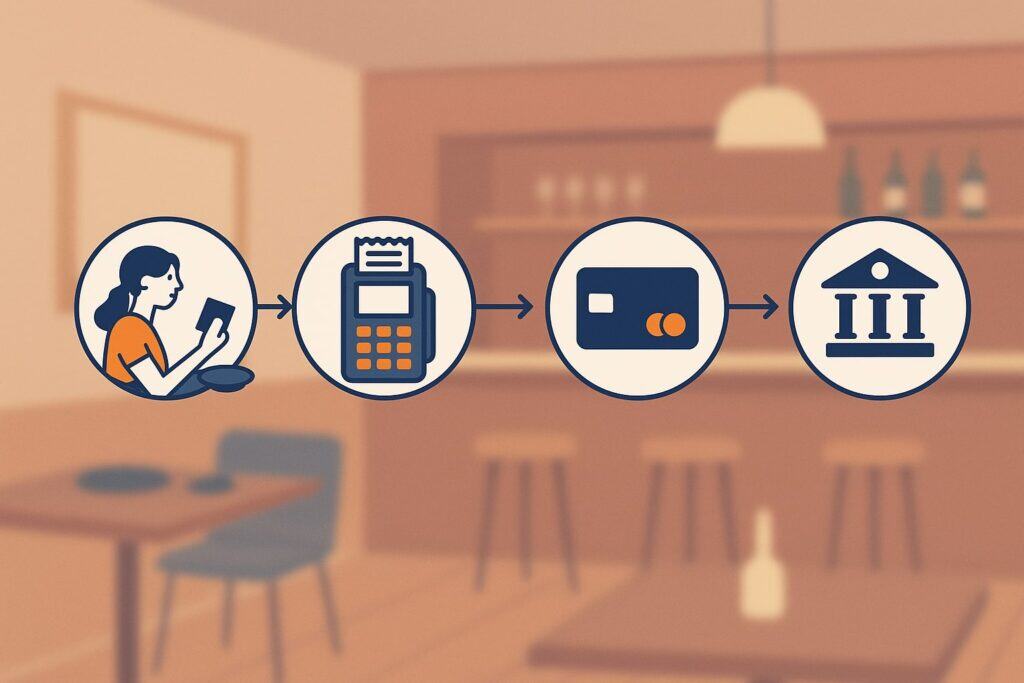

Restaurant payment processing is the end-to-end system that moves money from your guest’s wallet, card, or phone into your bank account.

It includes the hardware you put on the bar or on the table, the software in your POS, the payment gateway, the payment processor, the card networks, and the banks in the background. Together, they authorize each transaction, settle it, and deposit funds into your merchant account, while charging you various processing fees.

For a U.S. restaurant, this ecosystem usually starts with a restaurant POS (point of sale) or mobile payment device. That device connects to a payment processor or merchant service provider, which then communicates with card networks like Visa, Mastercard, American Express, and Discover, as well as your acquiring bank and the guest’s issuing bank.

When the system approves the transaction, the authorization code comes back to your POS in seconds and the guest’s payment is captured.

Modern restaurant payment processing also has to handle more than traditional card-present payments. Many restaurants now accept orders from online ordering platforms, first-party websites, mobile apps, QR codes, and third-party delivery marketplaces. Each of these channels creates its own payment flows and fee structures.

Because consumers now expect fast, digital, and contactless options, payment processing for restaurant environments is no longer just about “taking cards.” It’s about offering a mix of payment methods, integrating with your front-of-house and back-of-house systems, reconciling tips and taxes, and protecting sensitive card data.

If your restaurant payment processing strategy is fragmented or outdated, you’ll see it immediately in longer lines, frustrated guests, and staff that spend too much time fighting with the POS instead of serving.

How Restaurant Payment Processing Works Behind the Scenes

Restaurant payment processing might look simple from the guest’s side, but there’s a multi-step workflow behind every “Approved” message. Understanding this flow helps you choose better payment partners, read your processing statement, and spot issues before they cost you money.

At a high level, every payment goes through three phases: authorization, clearing, and settlement. Authorization happens in real time when the guest taps, dips, or swipes. Clearing happens when your POS batches those authorizations and sends them for processing, usually once per day.

Settlement happens when the cardholder’s bank sends funds (minus fees) through the network to your processor and then to your merchant account. Each step is influenced by the type of payment method used and the way you configured payment processing for restaurant operations.

The Key Players in Restaurant Payment Processing

In a typical U.S. restaurant payment processing setup, there are several core players involved in each transaction:

- Guest / Cardholder – The person paying with a credit card, debit card, digital wallet, or cash.

- Restaurant / Merchant – Your business, identified by a merchant account and MCC (merchant category code) specifically for restaurants.

- POS System / Payment Terminal – The device or software that captures card data and initiates the authorization request.

- Payment Gateway – The secure technology that encrypts and routes payment data from your POS to your processor, especially in e-commerce or online ordering flows.

- Payment Processor / Merchant Service Provider – The company that manages your merchant account, routes authorizations to card networks, and handles funding and chargebacks.

- Card Networks (Visa, Mastercard, etc.) – The networks that move transaction data between processors and banks and set interchange rates.

- Acquiring Bank – The bank that works with your payment processor to acquire funds from the customer’s bank on your behalf.

- Issuing Bank – The cardholder’s bank, which approves or declines transactions based on available credit, fraud checks, and other rules.

Restaurant payment processing is all about how efficiently these players communicate. If your POS is slow, your gateway is unreliable, or your processor’s risk filters are too strict, you’ll see more declines and voids at the table. If your acquiring bank and processor are slow to fund, cash flow suffers even when sales are good.

Because of this, it’s often better to think about payment processing for restaurant businesses as part of a single integrated stack rather than a random collection of devices and gateways.

Integrated payment processing can simplify reconciliation, reduce errors, support pay-at-table, and make upgrades like tap-to-pay or QR ordering much easier to roll out.

Step-by-Step Payment Flow in a Restaurant

Here’s what happens behind the scenes in a typical chip or contactless card transaction in a full-service restaurant:

- Order Entry – Your server enters items into the POS and prints a check or presents a tablet for review.

- Card Capture – The guest inserts, taps, or swipes their card, or uses a mobile wallet like Apple Pay or Google Pay.

- Authorization Request – The POS encrypts the card data and sends it to the payment gateway or directly to the processor.

- Network and Bank Check – The processor forwards the request to the card network, which routes it to the issuing bank. The issuing bank checks available funds, fraud signals, and card status.

- Authorization Response – The issuing bank sends back an approval or decline code. If approved, the restaurant gets an authorization code and the guest signs or confirms the total.

- Tip Adjustment – In the U.S., restaurants often adjust the final total after the guest adds a tip. The POS updates the authorization before settlement.

- Batching and Clearing – At the end of the shift or day, the POS sends a batch of all authorized transactions to the processor.

- Settlement and Funding – The processor submits transactions to card networks and acquiring banks, which move funds from issuing banks into your merchant account. Funding usually happens in 1–2 business days, but some processors offer same-day or next-day funding for restaurants.

This flow also applies to online orders, but the POS may be a web checkout or mobile app instead of a physical terminal. For online restaurant payment processing, you also need to handle card-not-present risk, 3-D Secure or similar tools, and higher base interchange for e-commerce.

If you understand this flow, you can better troubleshoot issues like repeated declines, high chargebacks, or delayed deposits. For example, if you’re seeing approvals but not getting funded, the problem is probably between your processor and acquiring bank, not your POS hardware.

Authorizations, Captures, Chargebacks, and Tips

Restaurant payment processing is a bit more complicated than retail because of tipping and how tickets are adjusted after authorization.

When the guest hands over their card, you’re usually running an authorization for the base amount of the bill. Later, after the guest writes in or chooses a tip, your POS sends a tip adjustment within the allowed time window.

If the tip pushes the total slightly above the authorization, most issuers allow a small tolerance. But if the adjustment is too large or too delayed, your processor can reject it.

In that case, your staff may need to ask the guest to provide another card or handle the difference in cash. Good payment processing for restaurant workflows will support automatic re-auth for large tips or guide staff when adjustments fail.

Chargebacks are another critical part of restaurant payment processing. A chargeback happens when the cardholder disputes the transaction with their bank. Common reasons in restaurants include duplicate charges, wrong tip amounts, or disputes about food quality or unauthorized orders (for example, when a card is stolen and used at your bar).

The issuing bank temporarily reverses the transaction and asks your processor for evidence—signed receipts, order details, and other documentation.

If your processor and POS are well integrated, you can quickly pull receipts, timestamps, and even table numbers to fight unfair chargebacks. If not, you can lose the dispute simply because you don’t have the right data.

Modern restaurant payment processing systems also use fraud monitoring tools to spot suspicious patterns, such as multiple high-ticket authorizations on the same card in a short period.

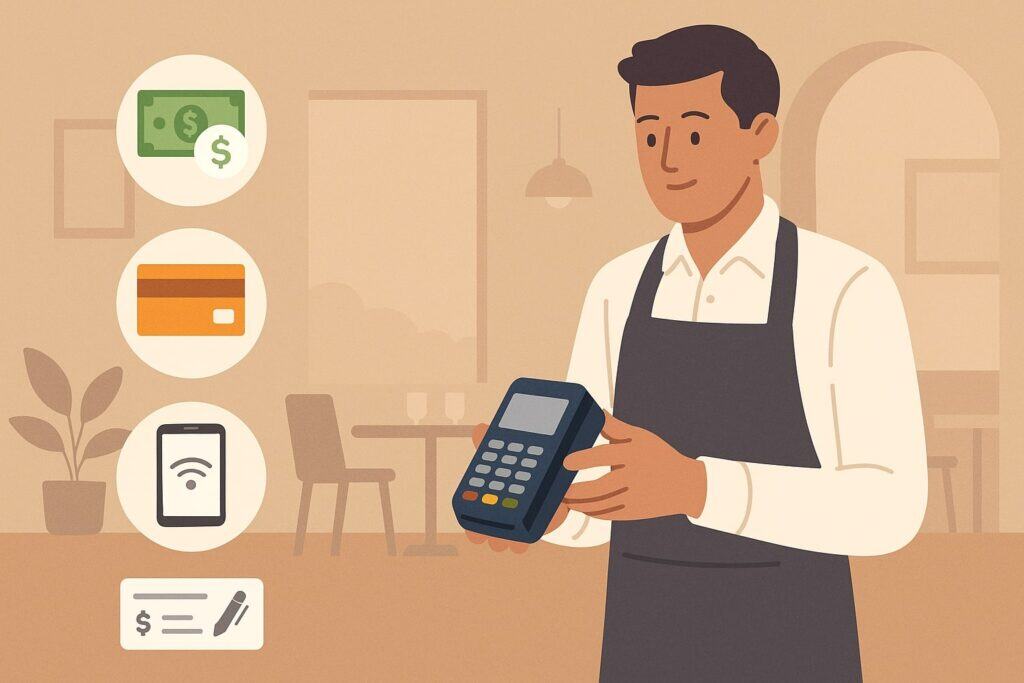

Core Payment Methods Every Restaurant Should Offer

The most successful U.S. restaurants treat payment choice like menu choice. Guests expect to pay with credit and debit cards, mobile wallets, and sometimes newer options like buy now, pay later. Cash is still important but shrinking, especially among younger diners.

When you evaluate payment processing for restaurant operations, you should start with the payment methods you’ll support today and over the next 3–5 years. The goal is to cover the most popular options for your local demographics while avoiding overly niche methods that add complexity without much volume.

EMV Chip and Contactless Card Payments

Chip cards (EMV) and contactless “tap” cards are the backbone of restaurant payment processing. In the U.S., contactless payments already represent a significant chunk of in-store card transactions, and their share has been growing rapidly since 2020.

For restaurants, EMV chip and contactless offer several advantages:

- Security – EMV generates dynamic transaction data, making it much harder to clone cards compared to old magnetic stripe swipes. Contactless uses the same EMV security plus near-field communication (NFC).

- Speed – Tap-to-pay and chip transactions typically take only a few seconds, which matters in quick-service and busy bars.

- Consumer expectation – Surveys show that a substantial portion of consumers now expect to use contactless methods and may avoid businesses that don’t offer them.

For restaurant payment processing, you should ensure every card terminal supports:

- EMV chip (insert)

- Contactless NFC for cards and mobile wallets

- Fallback magnetic stripe for rare edge cases

- PIN entry for debit cards, especially in quick-service

You can also consider pay-at-table devices, which let servers bring a wireless EMV/contactless terminal directly to the table. This avoids walking away with the guest’s card, increases perceived security, and can speed up table turns.

Handheld EMV/contactless devices are becoming more affordable and are now offered by major providers like Square and others, optimized for restaurant workflows.

Mobile Wallets and Tap-to-Pay at the Table

Mobile wallets like Apple Pay, Google Pay, and Samsung Wallet are now mainstream in the U.S. Digital wallets account for a growing share of point-of-sale and e-commerce payments, and many younger diners prefer to pay with a phone or smartwatch instead of a physical card.

To accept mobile wallets in your restaurant payment processing setup, you typically only need:

- NFC-enabled terminals (for in-person tap)

- A payment processor and POS that support network tokenization and wallet transactions

- Proper configuration so receipts and tips work smoothly with wallet transactions

Tap-to-pay on iPhone and Android also opens new possibilities. With Tap to Pay on iPhone, for example, restaurants can accept contactless payments using just an iPhone and a supported payment app—no extra hardware.

This can be a powerful option for:

- Food trucks and pop-ups

- Outdoor patios and events

- Line-busting during peak times

- Curbside pickup and parking-lot service

You’ll want to make sure your mobile wallet flows handle tips clearly. Many restaurant payment processing systems prompt for a tip directly on the tap screen, then send an electronic receipt. If you rely heavily on digital wallets, ensure your tipping prompts are fair but not pushy, especially as U.S. consumers are becoming more sensitive to “tip fatigue.”

Cash, Gift Cards, and Alternative Tender

Even as digital options grow, U.S. diners still use cash, especially in certain demographics or smaller towns. Cash usage is shrinking overall, but it isn’t disappearing, and emergency outages can make it essential.

Your restaurant payment processing strategy should include:

- Reliable cash handling – Secure cash drawers, clear procedures for cash drops, and reconciliation processes at shift end.

- Restaurant gift cards – Private-label gift cards integrated into your POS can drive repeat visits and act like stored-value accounts.

- House accounts and tabs – For bars, regulars, or corporate clients, house accounts with invoice-based settlement are still popular. These should be integrated with your payment system to avoid manual error.

It’s also worth deciding whether you’ll accept checks or money orders, though many modern restaurants have phased them out due to fraud risk and processing time.

As you introduce advanced restaurant payment processing tools, you may find that cash and checks fall below 10–15% of volume, but keeping support for cash at a minimum remains important for inclusivity and resilience during network outages.

Modern Digital Trends in Payment Processing for Restaurant Businesses

Today’s restaurant payment processing isn’t just about card machines at the counter. It’s about integrated digital experiences—QR ordering, kiosks, loyalty apps, and omnichannel payments that connect dine-in, takeout, and delivery. Restaurants that lean into these trends report higher average tickets, better data, and more repeat visits.

QR Code Menus, Order-and-Pay, and Self-Service Kiosks

QR code menus and order-and-pay flows exploded during the pandemic and are still widely used, especially in casual dining, breweries, and food halls. In this model, each table has a unique QR code.

Guests scan the code, browse a mobile menu, place orders, and pay from their phone. QR code payments are already used by more than a third of restaurants, and adoption continues to rise.

For payment processing for restaurant businesses, QR ordering changes a few things:

- Card-not-present risk – Even though the guest is physically in your dining room, QR payments run as e-commerce transactions, typically at slightly higher interchange rates than card-present transactions.

- Ticket structure – Some systems keep a running tab linked to the QR code so guests can add items before closing out.

- Tipping UX – Tip prompts appear on the mobile checkout screen, which can be tuned to encourage fair but not aggressive tipping.

Self-service kiosks follow a similar pattern but are physically installed in your venue. Guests place orders, pay, and then pick up food when it’s ready. Kiosks rely on the same restaurant payment processing stack as your front counter but may have dedicated merchant accounts or device IDs for tracking performance.

While some guests miss traditional server interactions, many appreciate the speed and control of self-service. When you’re designing restaurant payment processing, consider offering both server-led and self-service options, especially in quick-service or fast-casual concepts.

Online Ordering, Delivery, and Omnichannel Payments

If your restaurant accepts orders through a website, app, or delivery marketplace, you’re already running an omnichannel payment environment. The challenge is coordinating all those flows so they feed into a single reporting and reconciliation system.

Key considerations for online restaurant payment processing include:

- First-party vs. third-party – Orders through your own website or app give you more control over fees, branding, and data. Marketplaces may charge high commissions and handle payment processing themselves.

- Saved cards and wallets – Many guests like to save their cards or use wallet profiles so reorders are one-tap. This requires secure tokenization and PCI-compliant storage.

- Consistent pricing and fees – Make sure delivery and pickup pricing and any service fees are clearly disclosed to avoid chargebacks and regulatory scrutiny.

- Omnichannel loyalty – Integrating online and in-person payment processing for restaurant guests allows your loyalty program to track visits and spend across all channels.

Ideally, your restaurant payment processing provider will support an omnichannel gateway that connects in-store POS, online ordering, and app payments. That way, you can see a unified sales and fee picture and avoid juggling multiple merchant accounts that are hard to reconcile.

Subscriptions, Memberships, and Stored Payment Credentials

One of the newest frontiers in restaurant payment processing is recurring revenue. Some U.S. restaurants now offer memberships, coffee subscriptions, or special tasting clubs. Guests pay a monthly fee in exchange for discounted items, priority reservations, or exclusive events.

To support these models, your payment processing for restaurant operations must handle:

- Recurring billing – Automatic monthly or weekly charges on stored payment methods.

- Card updater services – Automatic updates when cards expire or are reissued, reducing failed payments.

- Proration and plan changes – When guests upgrade, downgrade, or pause memberships.

The same technology can power house accounts or corporate catering programs, where clients keep a card on file and are billed automatically after each event. As subscription and membership models grow, expect more restaurant payment processing platforms to add built-in recurring billing and invoicing tools.

Fees, Pricing Models, and How to Lower Restaurant Payment Costs

For many restaurants, card processing fees are one of the largest non-labor expenses. Small differences in rates and terms can translate into thousands of dollars per year. That’s why understanding pricing models is crucial when you compare restaurant payment processing providers.

Most U.S. processors use one of three pricing models: flat-rate, interchange-plus, or tiered (also called bundled). Each impacts how much you pay and how transparent your statement is.

Interchange, Markups, and Typical Restaurant Rates

Every card transaction includes interchange, the base fee set by card networks and paid to the issuing bank. Interchange varies by card type (debit vs. credit, rewards level), transaction method (chip vs. keyed), and merchant category (restaurants have their own codes). On top of interchange, processors add assessments from the networks and their own markup.

In interchange-plus pricing, you pay the actual interchange cost for each transaction plus a fixed markup (for example, 0.25% + $0.10). This is usually the most transparent model and is popular for serious restaurant payment processing with higher volumes.

Flat-rate models (for example, 2.6% + $0.10 for all in-person transactions) are simple and predictable but may be more expensive at scale. They are often used by all-in-one POS providers aimed at small or new restaurants.

Tiered pricing groups transactions into “qualified,” “mid-qualified,” and “non-qualified” buckets, which can hide higher costs for certain types of cards or transactions.

For most U.S. restaurants, effective blended rates for in-person payments often land somewhere in the 2–3% range plus per-transaction fees, though exact numbers depend on card mix, average ticket size, and negotiation.

Surcharging, Cash Discounting, and Service Fees

Because fees are so high, many restaurants explore programs that pass some or all processing costs to customers. The main options are surcharging, cash discounting, and service fees.

- Surcharging – Adding a fee when customers pay with a credit card. Visa notes that merchants in most U.S. states can add a surcharge to credit card transactions, but not debit cards, and must follow rules about disclosure and cap amounts.

- Cash discounting – Advertising a higher “regular” price and offering a discount for cash. This approach has different legal and card-brand implications than surcharging.

- Service or convenience fees – Flat or percentage fees applied to certain types of transactions, such as online orders or delivery.

State laws on surcharging and related fees are evolving. Some states explicitly restrict surcharges, while others allow them with strict transparency rules. New York, for example, tightened its law in February 2024, capping surcharges at the actual processing cost and requiring clear upfront price disclosures.

Before implementing any surcharge, cash discount, or fee program in your restaurant payment processing setup, you should:

- Consult a knowledgeable attorney or compliance expert.

- Verify the latest state-by-state rules.

- Notify your processor and card brands, if required.

- Train staff to explain the program clearly and consistently.

If done poorly, these programs can create negative customer reactions and increase chargebacks. Done correctly, they can protect your margin in an environment of rising interchange and inflation.

Negotiating with Providers and Avoiding Hidden Costs

When you evaluate payment processing for restaurant operations, don’t focus only on the headline rate. Consider:

- Monthly account fees

- Statement and PCI “non-compliance” fees

- Chargeback and retrieval fees

- Early termination and liquidated damages clauses

- Hardware lease terms

Many restaurants overpay because they’re locked into long contracts with expensive terminal leases and opaque tiered pricing. To reduce costs:

- Ask for interchange-plus pricing with transparent markups.

- Avoid long-term non-cancelable hardware leases; buy hardware or use month-to-month arrangements where possible.

- Review monthly statements for junk fees and negotiate them down.

- Consolidate providers so that POS, online ordering, and restaurant payment processing are integrated, reducing gateway and integration costs.

Security, Compliance, and Risk Management

Every restaurant that accepts cards must protect cardholder data and comply with industry security standards. Beyond legal and network requirements, strong security is simply good business—it prevents devastating data breaches, fraud, and reputational damage.

In payment processing for restaurant environments, security revolves around PCI DSS, encryption, tokenization, and fraud controls. With PCI DSS version 4.0 becoming fully mandatory, restaurants need to understand what’s changing.

PCI DSS 4.0 for Restaurants

The Payment Card Industry Data Security Standard (PCI DSS) is a global set of requirements for any business that stores, processes, or transmits cardholder data.

Version 4.0, which becomes fully enforced for most requirements, introduces stronger expectations around continuous risk management, authentication, and e-commerce security.

Key themes relevant to restaurant payment processing include:

- Stronger authentication – Expanded use of multi-factor authentication (MFA) for administrative access to systems handling card data.

- Ongoing risk analysis – Regular, documented risk assessments and “targeted risk analysis” for controls like password policies and log reviews.

- E-commerce payment page security – Tighter requirements for monitoring scripts on payment pages to prevent e-skimming attacks, important for online ordering.

- Improved access control – Clearer rules around who can access cardholder data and how access is reviewed and revoked.

For many smaller restaurants, the practical approach to PCI DSS under v4.0 is to reduce your card data footprint as much as possible:

- Use EMV and point-to-point-encrypted (P2PE) terminals so card data never touches your POS in clear text.

- Outsource online payments to hosted fields or redirects managed by your processor.

- Avoid storing card numbers yourself; use tokens and vault services instead.

Your restaurant payment processing provider should give you PCI documentation, SAQ (self-assessment questionnaire) guidance, and clear responsibilities for who handles what. If a provider can’t explain how they help you meet PCI DSS 4.0, that’s a red flag.

Reducing Fraud at the Point of Sale and Online

Restaurant fraud tends to fall into three buckets: stolen cards used in person, card-not-present fraud in online ordering, and internal (employee) fraud.

To reduce in-person fraud in restaurant payment processing:

- Make sure all terminals support EMV; avoid mag-stripe-only transactions.

- Train staff to check signatures or ID when something looks suspicious.

- Use pay-at-table devices so cards never leave the guest’s sight.

For online and QR-code orders:

- Enable AVS (address verification) and CVV checks.

- Consider 3-D Secure for higher-risk orders, even if it adds friction.

- Watch for patterns like multiple high-value orders to the same address with different cards.

Contactless payment scams, like so-called “ghost tapping” where scammers try to trigger unauthorized NFC payments in crowded spaces, have also drawn attention recently. While overall contactless fraud remains low relative to transaction volume, it’s wise to:

- Ensure staff never process tap-to-pay transactions without clearly showing the amount.

- Keep terminals under staff control rather than unattended in high-traffic areas.

Internally, basic controls like unique logins for each employee, regular void and discount report reviews, and clear tip procedures can dramatically reduce loss. An integrated restaurant payment processing system makes it easier to correlate payments, tips, and staff IDs to spot problems quickly.

How to Choose the Right Payment Processing for Restaurant Operations

Choosing restaurant payment processing is not just about picking the cheapest rate. It’s about selecting a partner and platform that fits your concept, volume, and growth plans. A food truck and a fine-dining group have very different needs, even though both accept cards.

Matching Payment Processing to Your Restaurant Type

Consider how your concept impacts restaurant payment processing requirements:

- Quick-service (QSR) – High transaction volume, low average ticket, speed is everything. You need fast chip/tap, self-service kiosks, and rock-solid uptime. Mobile wallets and tap-to-pay can significantly reduce line length.

- Fast-casual – Mix of counter and table service, often heavy on online ordering and pickup. Omnichannel integration and curbside flows become critical.

- Full-service – Complex tipping, split checks, and table management. Pay-at-table devices, tip adjust flows, and detailed reporting are key.

- Bars and nightlife – Tabs, pre-auths, and chargeback risk require strong card handling, ID checks, and fast terminals that work in low-light, crowded environments.

- Food trucks, pop-ups, and markets – Mobility and offline capabilities matter. Tap-to-pay on iPhone/Android or lightweight handheld POS devices can be ideal.

As you evaluate payment processing for restaurant needs, map features to your real workflows: How do you start a tab? How do you handle large parties? How often do you split checks? How many orders come from delivery apps? Your processor and POS should support these patterns without clunky workarounds.

Must-Have Features in a Restaurant POS and Processor

When you choose a restaurant payment processing stack, look for:

- EMV and contactless support across all terminals

- Integrated tip management (including pooled and individual tips, auto-gratuity, and simple tip adjustment)

- Pay-at-table and handhelds for full-service environments

- Online ordering and delivery integration (first-party and, if needed, third-party connectors)

- Real-time reporting and analytics for sales, tips, and fees

- Support for loyalty, gift cards, and memberships

- Omnichannel tokenization so saved cards can be used in-store and online

- Transparent pricing and contract terms

- PCI DSS 4.0–ready security features such as P2PE, tokenization, and strong authentication

Finally, assess support quality. Restaurant payment processing problems often happen at the worst possible times—Friday nights, holidays, or bad weather days when online ordering spikes. 24/7 support, fast terminal replacement, and clear incident communication can matter more than a few basis points of savings.

The Future of Restaurant Payment Processing in the US

Looking forward, restaurant payment processing will continue to move toward more contactless, mobile, and invisible payments. Global contactless payments are projected to keep growing rapidly through 2028, and many experts expect contactless to dominate in-store card transactions.

For U.S. restaurants, likely trends include:

- More tap-to-pay everywhere – As more terminals and phones support NFC, guests will expect to tap not just at the host stand but at the table, curbside, and even at events.

- Higher digital wallet adoption – Digital wallets are already taking a growing share of POS and e-commerce payments. Younger consumers in particular will expect Apple Pay, Google Pay, and similar options by default.

- Deeper integration with restaurant tech – Payment processing will be more tightly integrated with inventory, kitchen display systems, labor scheduling, and loyalty. Payments data will drive marketing and menu engineering.

- More real-time and instant payouts – Some processors already offer same-day or instant funding; this will likely become more common, supporting cash-flow-sensitive operators.

- Tighter security and compliance expectations – PCI DSS 4.0 is just the beginning. Expect more emphasis on ongoing risk analysis, e-commerce script monitoring, and advanced authentication, especially as card-not-present transactions grow.

At the same time, consumer backlash against excessive fees and tipping prompts may push restaurants to balance “smart” payment experiences with respect for guests’ wallets. Clear, honest communication about pricing, tips, and optional fees will become as important as technology itself.

Frequently Asked Questions

Q1. How do I set up restaurant payment processing for a new restaurant?

Answer: If you’re opening a new venue, setting up restaurant payment processing should be part of your pre-launch checklist, right alongside licenses, permits, and staffing. The basic steps are:

- Define your concept and payment flows – Decide whether you’ll be quick-service, full-service, or hybrid; if you’ll offer online ordering, delivery, or catering; and whether you need pay-at-table or kiosks. These decisions heavily influence your payment processing for restaurant requirements.

- Choose a POS with strong restaurant features – Look for table management, menu modifiers, tipping tools, and integrations with kitchen display systems and online ordering. The POS you pick often determines which payment processing partners are available.

- Apply for a merchant account or set up with an all-in-one provider – You can either work with a traditional merchant service provider that plugs into your POS, or use an all-in-one solution where the POS vendor bundles payment processing for restaurant merchants into a single package.

- Get approved and install hardware – Once underwritten, you’ll receive terminals, handhelds, or tap-to-pay apps. Ensure all devices support EMV and contactless.

- Configure menus, taxes, and tips – Before opening, configure sales tax rates, automatic gratuity rules, and suggested tip prompts. Test different flows like split checks and refunds.

- Complete PCI and security setup – Fill out the required PCI DSS SAQ, enable encryption and tokenization, and ensure your staff logins and permissions are configured securely.

Plan to run test transactions, including refunds and tip adjustments, before your soft opening. It’s far easier to fix restaurant payment processing problems when the dining room is empty than during a Saturday rush.

Q2. What payment methods should my U.S. restaurant accept in 2025?

Answer: For most U.S. restaurants, a best-practice mix of payment methods includes:

- Credit and debit cards via EMV chip and contactless – These remain the dominant in-person payment methods nationwide.

- Mobile wallets – Apple Pay, Google Pay, and others, accepted via NFC-enabled terminals.

- Cash – Even though cash usage is declining, it’s important for inclusivity and resilience during outages.

- Online card payments for web and app orders – With support for saved cards, wallets, and possibly buy now, pay later if it fits your concept.

- Gift cards and loyalty balances – Integrated directly into your POS.

You can consider additional options like bank transfers or instant pay solutions, but they’re not yet standard for most restaurant payment processing in the U.S. Crypto payments, while trendy in headlines, still represent a niche and may add more complexity than value for typical restaurants.

The bigger priority is ensuring you execute the core options well: fast EMV/contactless acceptance, smooth mobile wallet flows, and frictionless online payment experiences that align with your brand. If those work reliably, you’ll meet the expectations of the vast majority of U.S. diners.

Q3. How much should I expect to pay in restaurant payment processing fees?

Answer: Actual fees depend on your provider, pricing model, card mix, and average ticket size, but you can estimate:

- In-person card transactions – Often around 2–3% of the transaction amount, plus a per-transaction fee (for example, $0.05–$0.15), when using interchange-plus or competitive flat-rate pricing.

- Online and QR payments – Usually slightly higher than card-present due to increased fraud risk and interchange.

- Additional fees – Monthly account fees, PCI compliance or non-compliance fees, chargeback fees, and hardware costs.

To keep restaurant payment processing costs under control:

- Favor interchange-plus pricing where possible for transparency.

- Avoid long-term terminal leases; buy hardware or use flexible options.

- Ask providers to remove or reduce junk fees.

- Compare not just rates but total effective cost and support quality.

Over time, review your statements and look at effective cost as a percentage of gross card volume. If your effective rate creeps up significantly without explanation, it may be time to renegotiate or explore a new provider.

Q4. How will PCI DSS 4.0 and future regulations affect my restaurant?

Answer: PCI DSS 4.0 and evolving state and card-brand rules mean restaurants must take a more proactive, continuous approach to security and compliance. By March 31, 2025, most future-dated PCI DSS 4.0 requirements become mandatory, including stricter MFA, risk analysis, and e-commerce script monitoring.

Practically, this means:

- You’ll need to show ongoing security practices, not just annual checklists.

- E-commerce and online ordering flows will need better controls against e-skimming and script tampering.

- Password and access control policies will need to align with the updated standards.

Other rules, such as state surcharge laws and consumer protection regulations, may also evolve. New York’s 2024 update to its surcharge law is one example of how state rules are tightening around transparency and fee caps.

To avoid getting overwhelmed, choose restaurant payment processing and POS providers that actively track these regulations and provide clear guidance, updates, and tools. The right partners will help you stay ahead of changes instead of scrambling to react after a compliance deadline has passed.

Conclusion

Restaurant payment processing has become a strategic part of running a successful U.S. restaurant. It’s no longer just a card terminal on the bar—it’s a network of POS systems, mobile devices, gateways, processors, and banks that together shape how guests experience your brand and how fast you get paid.

When you design payment processing for restaurant operations, think holistically. Offer the payment methods your guests expect: EMV chip, contactless cards, mobile wallets, online ordering, and QR or kiosks where they make sense.

Choose a POS and processor with restaurant-specific features like table management, tip controls, and pay-at-table options. Demand transparent pricing and avoid long-term hardware traps and hidden fees.

Equally important, invest in security and compliance. With PCI DSS 4.0 and rising fraud risks, restaurants that protect card data and follow best practices will be better positioned to avoid breaches, fines, and reputational damage.

Finally, keep an eye on the future. Contactless and digital wallets will keep gaining ground, instant payouts will become more common, and integrated data will help you personalize offers and optimize your menu.

If you build a flexible, modern restaurant payment processing foundation today, you’ll be ready to adopt new payment methods and business models tomorrow—without tearing everything up and starting over.